Tharp's Thoughts Weekly Newsletter

-

Article: Computer Games Part 2 by Ivan Obolensky

-

Workshops: $700 Early Enrollement Discount ENDS TODAY!

-

-

Tip: A Key Factor Keeping the Market Afloat by D. R. Barton, Jr.

-

$700 Early Enrollment Discount ENDS TODAY!

Day Trading Systems and

Trading in Bear Markets and Down Markets

New Bonus Offer:

For Day Trading Attendees — 1 free year of Ken's Chatroom for Traders.

For Live Attendees — 1 free year of monthly coaching from Ken.

Day Trading and Live Day Trading with Instructor Ken Long

Learn two complimentary trading systems (and trade them on a simulator in class!) that are great performers in volatile market conditions like we are experiencing right now!

SPECIAL BONUS — One Year Free Membership in Ken's Powerful Chatroom

Inspired by the powerful networking Ken has seen develop over the years at VTI, both through the Super Trader program and workshop attendees,he has created and leads a chatroom of active traders with a shared interest in swing trading and intraday trading.

Here’s what one chatroom member recently wrote:

I use Ken’s chat room daily. It has refined my technical trading skills immensely. As I study other trader’s trades alongside my own, I am able to make regular improvements … the folks in the trading room are friendly, insightful and smart. They work hard every day and share what they learn freely with others in the room. I am thankful for this forum.—M. Milbradt

Live Day Trading — November 9-10

The three-day Day Trading Workshop is the classroom training course, and the Live Day Trading Workshop is the complementary, in-the-field learning experience where students have a master trading coach by their side and have the chance to apply the trading concepts in the real world. It is unlike any other workshop offered by the Van Tharp Institute. You craft your own daily trading plan based on Ken Long’s Frog, RLCO, or swing system signals and trade your own platform with your own money—all under the guidance of Ken, who will offer thorough direction and individualized feedback.

SPECIAL BONUS — Free year of monthly coaching webinars from Ken to Live Trading Students

In your monthly coaching group call Ken will cover:

| |

1. |

A review of your performance stats |

| |

2. |

Feedback on your routine performance of the tasks of trading |

| |

3. |

Progress and management for your stated goals |

| |

4. |

Your feedback on your accountability to your trading partner |

| |

5. |

Answers to your questions on systems and techniques |

Trading in a Bear Market and Down Markets with Instructor Mark McDowell

Learn how to identify, prepare for, trade during, and profit from the next big bear market—or from any smaller market that’s heading down.

This workshop helps you learn how to think about trading broad bear markets and trading an asset class, sector or even one symbol that is moving down in bear mode. For a major bear market, think equities in 2008-2009. For a down move, think oil in 2014-2015. Imagine having had some ways you could have effectively traded those periods. Major bear markets don’t come that often but “lesser” down moves can be found almost anytime – including during bull markets. Start using the information from this workshop when you return back home — and also be prepared for the next big bear market.

| • |

|

Study in depth the concept of a bear market. |

| • |

|

Learn what a bear market truly is and learn several ways to define and measure the bear market type. |

| • |

|

Know when a bear market type might be starting and how to know when it might end. |

| • |

|

Learn 5 trading strategies suited for bear market conditions. |

| • |

|

Learn how options can be especially useful for bear market types. |

To register or to see the full workshop schedule, click here.

When you attend both three-day workshops you get an additional $500 discount.

Feature Article

Computer Games

Part 2

by Ivan Obolensky

Click here to resolve formatting problems

Last week Ivan covered the origins of HFT—High Frequency Trading. Over time the switch in the marketplace to computer trading created several game changing events. Last week's article brought us up to the new millennium. Click here to read Part 1 if you missed it.

By the year 2000, two events happened that once again greatly influenced both the market and the infrastructure that supported it. The first was the bursting dot-com bubble, and the second was, once again, a regulatory fix.

Several new rules were put together, the first of which was decimalization. Stocks previously traded in minimums of 1/8th (12.5 cents), or even a 1/16th (6.25 cents), rather than simply 0.12 or 0.06. Regulators decided that it was in the best interests of the public that stocks be quoted in decimals rather than these archaic fractions left over from past centuries. The rule would drive the spread from the minimum 1/16th (6.25 cents), as per the above example, to a penny, saving the consumer money.

Decimalization had two consequences. The first was that spreads narrowed, which benefited the consumer. The second was that many market-makers were driven out of business. The spreads were too narrow for them to make a living. Taking their place were more Electronic Communication Network (ECN) platforms. They sprouted everywhere. There was no coordination, just tons and tons of data. It became extremely difficult for a broker to make sure he got the best price for his customer because of the rising number of ECN venues.

Shortly thereafter, a new set of regulations was implemented called Regulation National Market System, or Reg NMS. This set of rules required broker-dealers to access the very best price available before executing a trade, or risk fines and sanctions. By ordering that all broker-dealers have access to every available quote, they indirectly mandated that all market venues be interlinked. Again regulators felt that this could only benefit the public, but this created difficulties for those who placed trades for the consumer. The first was that all broker-dealers who traded for the public had to monitor thousands of stocks on hundreds of venues all the time. Trades sent to be executed were often put in queues awaiting their turn, but if prices changed while waiting in the queue they had to be re-routed to another venue to get the better price. There, the same process repeated. Orders could take much longer to execute, and the price of waiting could be expensive as those at the front received the better price and the trade was bumped to another queue that offered the best one but at a less advantageous price. Unless one knew how to place an order exactly in the language that the computer networks understood, executions could happen at prices different than what was expected. But there was one group that understood the significance of this and how to manage their orders so they didn’t get bounced - the electronic traders that flowed a lot of business to these electronic platforms.

While the markets were retooling, traders had grown in sophistication. Their everyday computers were replaced with the fastest technologies available. Programmers fine-tuned small programs called algorithms (algos) which consisted of several logic steps parsed in computer language. A simple algo might be “If the price is greater than 10.25 then offer to sell 100 shares. If the price is less than 10.00 offer to buy 100 shares”.

Traders using algos could take advantage of the price discrepancies between the thousands of quotes that were now available to be processed.

Over time the algos grew much more complex so they could adapt to multiple situations. Since many of the traders generated the volume the ECNs needed, they also became privy to the type of order entry that could jump to the head of the queue, buy at a lower price, and then sell it at a higher price to the order waiting behind it. Secondly, by offering to buy and sell, the electronic trader created liquidity and therefore could earn the liquidity-maker fee of 0.003 cents per share if their order to buy or sell was executed. By analyzing all the available quotes, the algos made sure their offer to buy or sell was the best available, even if the algo simply made no profit on the trade. The trick was to offer liquidity across the market and earn the fee. It was risk-free and if one could trade a billion shares a day, it was also extremely lucrative.

This meant that electronic traders required speed, the fastest possible speed available. They coveted ‘low latency’. Latency is the time it takes to run an order from a computer to the ECNs that matched and executed the trade. Exchanges and their ECNs began to rent server space next to their own servers so trading firms that wanted the fastest execution of trades possible could do so. This also required that the algos that offered liquidity, jumped order queues, or executed trading strategies be fully automated. Trading institutions researched machine learning (see Artificial Intelligence and Language) that raised the complexity of algos to a new level. Algos were programmed to change their executions with changing market conditions.

Meanwhile institutions had not stood still during this time. They needed to buy and sell large numbers of shares without having to pay the higher prices the queue-jumping algos made them pay by buying the shares first and reselling them to the institution at a higher price. They built computer systems of their own and created different algos that now broke up large orders into small chunks and traded them across multiple venues in random patterns.4

If this sounds like the Wild West, or some kind of cyber war between dueling computer systems and programs on a micro level, you would be correct. Volume went through the roof. Eventually major investment banks such as Goldman Sachs and other financial institutions saw the profit potential and either bought existing ECNs for large sums, or built their own.

But there was a problem. It is called uncertainty. Uncertainty is the bane of HFTs because it increases volatility (price movement per unit of time). It is like noise on a phone line. Too much noise, and it is impossible to extract a signal. You hear only static. When volatility rises above a certain point, algos can make mistakes, and therefore, they have instructions to stop trading immediately and cancel all bids and offers.

What this means on the macro level is that in the event of a major shock that creates uncertainty and large volatility, HFTs will shut down their trading system. What happens to all the liquidity that was being offered just seconds ago? It evaporates. What happens to stock prices? They drop. They drop hard.

Conclusions and Observations:

| |

1. |

Regulation even with the best of intentions often leads to unforeseen consequences. This is not to say that there should be no regulation, but rather that those who regulate must be aware that regulations can create as many problems as they solve. As a rule, regulation is best in small doses. |

| |

2. |

With the lure of big money it is likely that competition between HFTs will intensify causing some to go out of business. Note that the NYSE volume of HFT trades has decreased from 60-70% in 2006 to 50% as of 20125. It is possible that overall HFT volume has peaked although it is highly unlikely HFTs will disappear anytime soon. They are now necessary under the current market framework simply because exchanges need the volume that HFTs provide to survive as for-profit entities. Note: Exchanges were not always for-profit publicly traded companies that depend on order volume to remain viable. The NYSE was recognized as a Not-for-Profit organization in 1971 but became for-profit in 20056. |

| |

3. |

In the same way, HFTs need the exchanges and the liquidity maker-fees exchanges offer in order to make money. It is a symbiotic relationship. One can’t exist without the other. |

| |

4. |

As an observation, with so many HFTs in competition today, the easy money has probably already been taken. New HFTs will find it more difficult to make the profits needed to justify the effort and outlay for new systems. Of course, if an HFT trading group can create systems that operate at the nanosecond level, then they have the advantage and the cycle repeats. Regardless, there is a limit to data speed, and that limit is the speed of light. |

| |

5. |

Complexity theory points out that highly networked entities are prone to create wide market swings similar to the population changes in predator-prey relationships. In spite of this tendency, such networks are extremely robust and tend to correct back the other way rather than simply collapse7. The flash-crash of the US market in the summer of 2010 is such an example. |

| |

6. |

Referencing complexity theory again, it is likely that volatility will increase going forward. This brings up the most interesting and unknown factor of HFTs. HFTs reduce the spread between the bid and ask, which damps down short-term volatility; however, if volatility is a natural phenomenon inherent in all system interaction, similar to noise on signals, or the vibrations of molecules, damping it down in one form can lead to more volatility in another, similar to taking two pieces of bread with jam in the middle and pressing them together. The jam leaks out the sides and makes a mess. |

| |

7. |

In and of themselves, HFTs are not inherently bad; they operate at such a small time scale they do not often affect those trading on a longer time frame with some exceptions. Algos can create order imbalances by generating many large orders above, or below, the market that trick other traders into anticipating a move higher, or lower. The orders are then canceled when the market starts to move. This is called spoofing and is illegal8. Although this a danger, the mutually supporting close relationship between HFTs and exchanges is perhaps the greater one. The vested interest to maintain the relationship at any cost could prove hard to unravel if required. Secondly, if a choice must be made between the public and that relationship, it is not difficult to predict which way the decision will go. |

| |

8. |

Institutional traders have also gotten into the Algo game by spreading out their orders across multiple venues at multiple times and in small order size reducing the impact of HFTs jumping the queue and taking advantage of the large order by buying first and selling to the large order behind them. The playing field is more even than it was. |

| |

9. |

Regulation is always the sword of Damocles that hangs over the heads of HFTs. What has been given can be taken away. |

HFTs are a factor in the investing/trading game and should be understood, but they are not the key player. Central Bank interventions to preserve market trends in the face of increasing debt ratios and tepid economic fundamentals are the elephant in the room. Comparatively, HFTs are small potatoes.

Still, if one sits down at a poker table, it is best to know who one is playing against.

Copyright © 2015 Ivan Obolensky http://www.dynamicdoingness.com

Ivan recently joined Dr. Tharp's Super Trader Program and we look forward to publishing more of his insightful articles.

| |

4. |

Patterson, cit. |

| |

5. |

A. (2012). Declining U.S. High-Frequency Trading. The New York Times. Retrieved September 11, 2015 from nytimes.com/interactive/2012/10/15/business/Declining-US-High-Frequency-Trading.html?_r=0. |

| |

6. |

A. (2015). NYSE History, The History of the New York Stock Exchange. Retrieved September 11, 2015 from stock-options-made-easy.com/nyse-history.html |

| |

7. | Page, S. E. (2009). Understanding Complexity. Chantilly, V.A.: The Teaching Company |

| |

8. |

Levine, M. (2015) Why is Spoofing Bad? BloombergView. Retrieved September 11, 2015 from bloombergview.com/articles/2015-04-22/why-is-spoofing-bad- |

Workshops

Combo Discounts available for all back-to-back workshops!

See our workshop page for details.

Free Book We're Giving You a FREE Book!

TRADING BEYOND THE MATRIX

The Red Pill for Traders and Investors

We pay for the book, you pay for shipping.

ALL YOU HAVE TO DO IS CLICK HERE!

Below is a brief video on how powerful this book is to traders.

Trading Tip

A Key Factor Keeping the Market Afloat

by D. R. Barton, Jr.

Click here to resolve formatting problems

Over the past few months, we’ve had a bunch of bad news about the global economy. Most notably,

| |

• |

China’s economic slowdown and equity market meltdown |

| |

• |

The commodity market dive, especially in industrial metals and the continuing weakness in crude oil |

| |

• |

Emerging market debt repayments (which are denominated in US Dollars) and associated currency wars due to the continued strength in the US Dollar |

| |

• |

The decline in U.S. corporate earnings with second quarter announcements showing negative year-over-year growth |

With all of this going on, the markets took a big drop in late August including a mini flash crash on August 24th. Since then the markets bounced back modestly in September, dropped again in early October to test the August lows and since then, have sprung to new multi-month highs.

Click here for larger image.

With All of the Negative Global News — What’s Holding the Market Up Now?

China’s economy hasn’t gotten any better recently. The US Dollar is in the same range it has been in since April. The emerging market debt situation is no less bleak that it was a few months ago. Yet the markets have retraced almost 80% of the down move since August and are currently holding at this higher level:

Click here for larger image.

What gives?

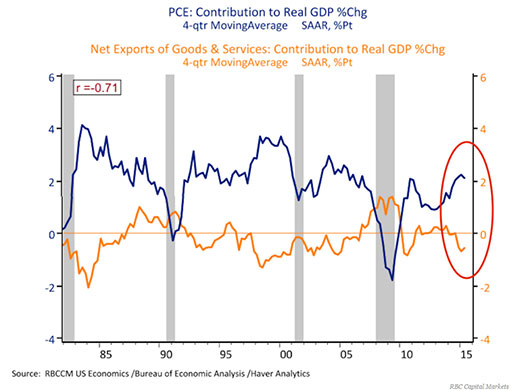

The U.S. consumer has stepped up spending big time. RBC Capital Markets chief US economist Tom Porcelli put out data showing that internal real consumption is fueling U.S. GDP growth. In the chart below, the blue line gives us consumption contribution to GDP growth while the orange line shows net exports:

Porcelli sums up the meaning of the chart nicely:

"One could argue that the global weakness this year has had some real effect on US trade, which has fallen on a trend basis to a lowly -0.55% contribution to topline GDP," writes Porcelli. "But the reality is that the entirety of this fallout has been offset (and then some) by the strengthening US consumer. The contribution to GDP from real consumption is now at 2.1% and up 0.8% from early 2014 (the last time trade was a 'neutral' contributor to topline growth."

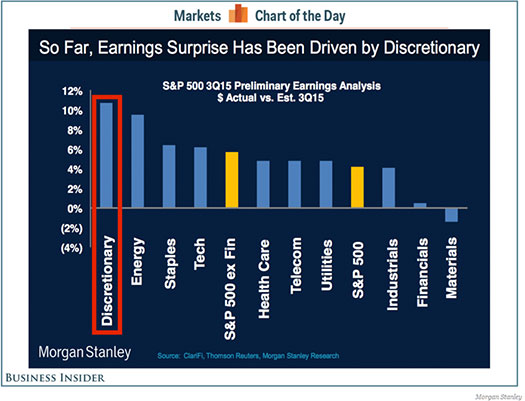

At a result — so far - Q3 earnings reflect consumer spending strength as you can see in this Morgan Stanley chart from a Business Insider story

Here we see that the first and third strongest earnings by market sector (through last Friday) have surprisingly been in Consumer Discretionary and Consumer Staples.

With the ongoing global economic slowdown competing against the continued U.S. consumer spending growth, so far the U.S. equity markets seem to be reacting more to the strong buying at home. The big question is whether this trend will carry over into the Christmas holiday season. Stay tuned…

As always, I love hearing your thoughts and comments about these areas. Send them all to drbarton “@” vantharp.com.

Great Trading,

D. R.

About the Author: A passion for the systematic approach to the markets and lifelong love of teaching and learning have propelled D.R. Barton, Jr. to the top of the investment and trading arena. He is a regularly featured analyst on Fox Business’ Varney & Co. TV show (catch him most Thursdays between 12:30 and 12:45), on Bloomberg Radio Taking Stock and MarketWatch’s Money Life Show. He is also a frequent guest analyst on CNBC’s Closing Bell, WTOP News Radio in Washington, D.C., and has been a guest on China Central Television — America and Canada’s Business News Network. His articles have appeared on SmartMoney.com MarketWatch.com and Financial Advisor magazine. You may contact D.R. at "drbarton" at "vantharp.com".

Swing Trading Systems E-Learning Course

The new Swing Trading Systems home study course is now available! Learn with Dr. Ken Long as he teaches his Swing Trading Systems Workshop via streaming video! The new Swing Trading Systems home study course is now available! Learn with Dr. Ken Long as he teaches his Swing Trading Systems Workshop via streaming video!

This new e-learning course includes Ken Long's Swing Trading Workshop, 5 swing trading systems and a bonus workshop featuring Van Tharp on Tharp Think principles. The course also includes extensive downloadable files to support your learning.

You can complete this course at your own pace, from the comfort of your own home or office, and access the materials as many times as you wish during your 1 year subscription period.

Take a look at this video from Ken to learn more about this course.

We have extensive information about the Swing Trading System e-learning course, including how to purchase...click the link below!

Learn More About The Swing E-Learning Course...

In the six minute video below, Ken analyzes several trades from the relatively quiet session on Monday, October 12. He opens with a swing trade that started last week on XIV talking about the entry, initial stop, target, and progress of the trade so far. That swing trade offers the opportunity trade XIV intraday with some confidence in the long bias. Ken provides two tradeable intraday scenarios for the XIV move during the Monday session and the position sizing ramifications for each. Ken then discusses a second trade where one of the traders in the chat room went short USO and earned a couple of R for the effort.

Matrix Contest

Enter the Matrix Contest Enter the Matrix Contest

for a chance to win a free workshop!

We want to hear about the one most profound insight that you got from reading Van's new book, Trading Beyond the Matrix, and how it has impacted your life. If you would like to enter, send an email to van@vantharp.com.

If you haven't purchased Trading Beyond the Matrix yet, click here.

For more information about the contest, click here.

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Send comments or ask Van a question by clicking here.

Also, Click here to take our quick, 6-question survey.

Back to Top

Contact Us

Email us at van@vantharp.com

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, e-mail us at info@vantharp.com.

To stop your subscription, click on the "unsubscribe" link at the bottom left—hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

Call us at: 800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute and the International Institute of Trading Mastery, Inc.

Be sure to check us out on Facebook and Twitter!

Back to Top |

|

October 28, 2015 #757

Our Mission

Van's Top-Twelve Favorite Trading Books

Van's Favorite Non-Trading Books

Viewing on-line eliminates spacing, and formatting problems that you may experience in your email program.

Ongoing Contest: Learn how you could win a $50 coupon and a grand prize of a free workshop!

www.youtube.com/vantharp

How are we doing?

Give us your feedback!

Click here to take our quick survey.

From our reader survey...

"I think the newsletter is

extremely generous and it is a resource I utilize constantly.

I have saved every single one

since I first subscribed."

Trouble viewing this issue?

View Online. »

Van Tharp You Tube Channel

Tharp Concepts Explained...

-

Trading Psychology

-

System Development

-

Risk and R—Multiples

-

Position Sizing

-

Expectancy

-

Business Planning

Learn the concepts...

Trouble viewing this issue?

View Online. »

Check out our home study materials, e-learning courses, and best-selling books.

Click here for products and pricing

What Kind of Trader

Are You? Click below

to take the test.

Tharp Trader Test

Back to Top

Introduction to Position Sizing™ Strategies

E-Learning Course

Perfect for auditory/visual learners who learn more effectively from an instructional format that is full of interactive features!

Only $149

Learn More

Buy Now

SQN® and the System Quality Number® are registered trademarks

of the Van Tharp Institute

|