Update on Cryptocurrencies: September 18th, 2022 By, Nolan Loxton

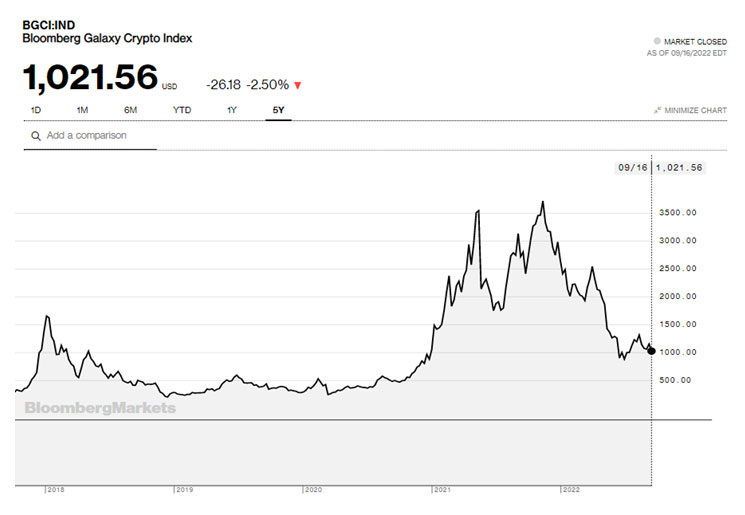

Bloomberg announced in May of 2018 that they had created a cryptocurrency index called The Bloomberg Galaxy Crypto Index. Since Bloomberg only caters to institutional clients, an index of this nature was one of the first steps toward widespread institutional involvement. The index composition changes regularly but we show the graph every month because so many institutional investors follow it.

This is the five-year chart for the index:

The index started in May 2018 at 1,000, reached a peak in May 2021 of 3,504, and then dropped significantly until June 2021. It set a new high on November 12th last year of 3,715 and since then has been sliding down until recently. After dipping below 1,000 in June and July, it bounced up to 1,292.13 with a minor series of higher highs and higher lows…so far. At the moment, the index is retesting the 1,000 level and it may retest the June lows.

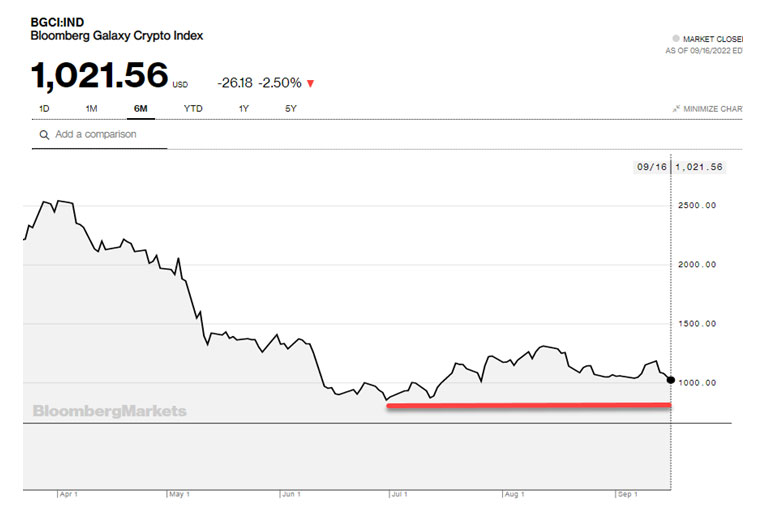

You can see the recent price action better in the six-month chart below:

Market Summary

a) Market type:

Bitcoin (BTC) hit a new all-time high of $68,789.63 on November 10th, 2021 but has had a sharp downturn since then erasing all of its gains back to November 2020.

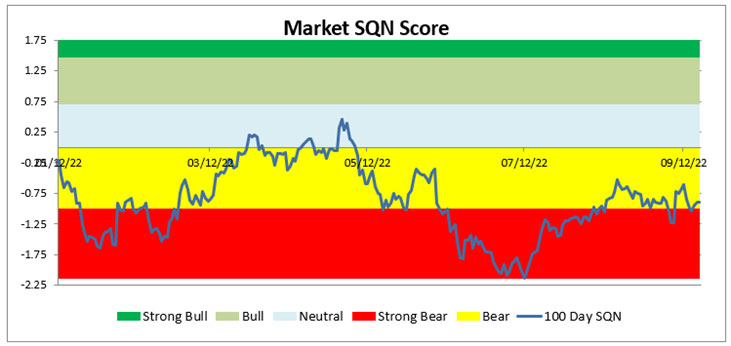

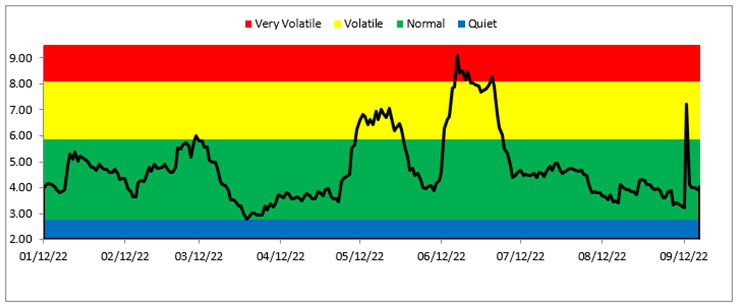

We are in a “Bear Normal” market type at the moment. The crypto market spent most of September in this market type although we did see one brief excursion into “Strong Bear Volatile” territory.

The following heatmap breaks down the crypto market by market capitalization of coins and indicates the calendar year-to-date performance. Bitcoin’s 57.83% YTD drawdown is its smallest crypto bear market since 2010. During 2018, the market corrected 72% and in 2014, BTC pulled back 62%.

Also note the size of the stablecoins (USDC, USDT, BUSB and DAI) market capitalization relative to ETH market capitalization. I write more about this factor later in the “Market in Pictures” section.

Courtesy of Coin360.com

b) Super Trader Bitcoin System

The objective of the ST system is to outperform a Bitcoin buy-to-hold while still allowing for restful nights.

The system entered its most recent BTC position on July 28th at $23,844 with an initial stop at $19,324. That gave us an initial risk amount of $4,520 per coin (1R). The BTC price moved, as did the trailing stop and we exited on August 19th at $22,631 for a loss of 0.27R. A fractional loss without disrupting sleep on any night.

If the BTC low in June were to hold, the system would likely trigger a reentry somewhere around the $25,000 mark. We’ll monitor BTC and I’ll update you in the October newsletter on any signals from the system.

c) Discussion: The Great White Stop

The Super Trader Bitcoin system stop getting hit and a recent holiday experience made me ponder the premise of the “Stop” more earnestly.

It was a beautiful September day and I was wriggling into a wetsuit in preparation for my “Swimming with the Seals” adventure. The skipper gave the usual snorkeling briefing focusing on currents, site hazards, and main attractions. He mentioned that the most important task for us on this particular snorkeling trip was to stay close to the boat. As he continued his instructions and as other adventurers inquired, I wondered for a moment if I misheard some unusual advice. Let’s jump to the dialogue:

Skipper: “…and if you hear this whistle (followed by him blowing a very loud whistle) get onto the boat – immediately.”

Wetsuit wriggler 1: “Why?”

Skipper: “There’s a Landlord inbound.“

Wetsuit wriggler 2: “A Landlord?”

Skipper: “A Rodney Fox, a Holy Mackerel, a Betty White, a White Pointer…”

Wetsuit wriggler 1: [sounding less than inspired] “Right…you mean a Great White Shark.”

Skipper: “Yeah.”

Wetsuit wriggler 3: “How do you know a shark’s coming?”

Skipper: “We’ve got a spotter on the mountain.”

Wetsuit wriggler 1: “How does he know a shark is coming?”

Skipper: “He’s got a good set of binoculars.”

Wetsuit wriggler 1: “How does he let you know if he sees one?”

Skipper: “Gives me a buzz on my phone – but don’t worry, the Landlord is not interested in you and we’ve never had a problem. To the boat!”

This seemed to put the wetsuit wrigglers collectively at ease and we were off to enjoy a breathtakingly wonderful experience. With 40-foot+ visibility in the crystal clear water, seals by the hundreds swam around all very interested in us. Mother Nature was in her full glory . . . and the spotter never saw a single Landlord.

Later that night, however, my mind was not at ease. As I lay in bed, a couple of contrarian thoughts crystalized in my mind:

- I agreed with Skip that sharks aren’t interested in humans.

- I acknowledged that the wetsuit camouflaged me some as just another seal swimming in the middle of a pod of seals.

- Any hungry shark of reasonable intelligence, however, would be expected to go for the lamest seal in the middle of the pod. I had been, therefore, an attractive target for a Landlord.

- That there had never been an incident before was comforting to a degree. Skip wasn’t bending the truth when he said this. He was 100% honest. In the sample of seal diving trips he had skippered, never had there been an “incident”. His sample, however, is not the population – just as the map is not the territory.

- The skipper’s exit plan for me was based entirely on his assumption that an “infringing” shark would be visible by the spotter from above the water and would be seen in enough time for us to get back on the boat. After thinking about that exit plan, however, I discovered that I was completely lost on some details of the plan such as:

Was the man on the mountain diligent for the entire time I was in the water?

Were his binoculars high quality?

Did he have the span of control to monitor all of the most likely visual angles?

Did he ever question the presuppositions of Skip’s plan?

I realized that evening that I had jumped in the water without remembering Mark Twain’s trap: “What gets us into trouble is not what we don’t know. It’s what we know for sure that just ain’t so.”

- If worst had come to worst, any reasonable reporter reporting the facts would not have been able to use the headline “Shark Attack” but merely “Shark served bad breakfast in usual spot”.

Now, back to the Super Trader Bitcoin system exit. What did I learn and reaffirm through the recent BTC trade?

The market is uninterested in the system’s position in the same way sharks are uninterested in humans.

The system found the entry criteria for a long position had been met while the market type was Strong Bear Normal. The system merely alerted me that for the past sample of descriptive statistics, BTC usually started moving upwards from the entry price levels and conditions. Statistically, I know the potential price recovery has an asymmetrical risk to reward ratio. This entry was not like swimming in a black wetsuit in the middle of a pod of seals, it was more like being in a shark cage—a reasonable endeavor for the risk averse.

The system’s descriptive statistics assumes there are various sharks out there in the big blue market, both seen and unseen. One of Van’s great nuggets of wisdom in the Peak Performance Home Study course is “there is a trade out there with your name on it”. I acted on the evidence the system provided in accordance with the rules and position sizing strategy. I took the signal, allowed the market some time and space to provide evidence and it did. Did the system jump back into the boat on a false alarm? Maybe. Will the system provide a reentry signal shortly? Maybe. More important are the following two questions: Will the system live to fight another day? Definitely. Will I come back to trade the system another day? Yes.

Any trader focused on improving his/her trading craft will happily log the following facts in their trading log and R-histogram.

d) News Map:

Context is all-important. To add some context to recent news events we will focus our attention on the five main types of players and the games they play in the crypto space.

We are leaning on a key Tharp Think principle here: “The map is not the territory. The better my map represents the territory, the better I will function in the world.”

We are not trying to explain the extremely complex, non-linear, open crypto universe but rather we look for a useful lens to identify what changes may be important affecting the ecosystem and ultimately, supply and demand. (What is “useful” for a trader? Tools that help make money.)

On our map, the main players and games are:

The HODLers:

These are mostly retail speculators with no trading systems or buy-and-holds with no stoploss. The early adopter HODLers have done quite well and with many who are still whales today. Many whales pivoted into other categories. The late adopters haven’t fared quite so well, they may be whales but their average BTC cost is underwater. For HODLers, 1 unit of risk (1R) represents their total capital committed—it’s basically an all-in bet. HODLers have no cash flow day to day without selling/staking the holdings.

The Traders:

These are large speculators such as hedge funds as well as the systematized disciplined retail traders. Their cash flow is dependent on the gains/losses in the underlying positions on positive expectancy systems. The common denominator amongst traders is a position sizing approach to capital allocation as well as a risk to reward approach at a trading strategy level (usually a minimum of 2:1 risk reward). For this reason, private equity and venture capital are also included in the Trader category as they have definite entries and exits as well as strict position sizing rules.

Business, Big and Small:

This includes the major commercial players who design blockchain infrastructure, have already adopted blockchain or are actively in the process of integrating blockchain and its related products and opportunities into their business models. Their cash flow originates from their usual business activity. Blockchain offers operational efficiencies improving cash flow and customer experiences.

For the small business, blockchain offers the opportunity to level the playing field (or should we say “paying” field) to unlock cash flow.

The Market & Makers:

This represents the market makers, brokers & exchanges (both traditional and DeFi), banks and asset managers. Cash flow is ongoing from volume in its various shapes of trading, spreads, commissions, assets under management and even order flow payments.

The Sheriff & Co.

This represents governments as well as any free market interventions in its various shapes, sizes and forms. The profit of all other players is their tax base and therefore cash flow, plus or minus the impact a couple of trillion, depending on the state of the printing presses.

With our main players categorized, let’s look at some noteworthy news items by category:

HODLers:

- MicroStrategy (MSTR), is selling $500m in new stock and will use the proceeds for general corporate purposes, including the acquisition of Bitcoin.

Traders:

- A new inverse ETF, the Rex Short MSTR ETF, will give traders the ability to easily short MicroStrategy, and in effect, to short BTC.

- The Chicago Mercantile Exchange launched ETH options trading and added Euro denominated ETH futures thus increasing the competition with the already pressured crypto exchanges.

- Cryptos have been unusually highly correlated with US stock markets lately. The one-year US Large Cap (SPY) correlation is at 0.71 versus the 5-year correlation of 0.36. That’s a further sign of institutional adoption.

Market Makers:

- Crypto exchanges are facing more competition as various other players enter the market. E.g., Fidelity is considering branching out their institutional crypto offering to individual investors and SEBA bank in Switzerland announced ETH staking. This offers investors the same exposure with less counterparty risk.

- Coinbase is funding a lawsuit against the U.S. Treasury department following the sanctions on the smart contract Tornado Cash. Coinbase CEO Brian Armstrong said in a statement that the Treasury went too far taking “the unprecedented step of sanctioning an entire technology instead of specific individuals.”

- Tether appointed BDO, the World’s fifth-largest accounting firm to issue assurance and attestation reports of its reserves.

Business, Big and Small:

- Depository Trust & Clearing Corp (DTTC) started live testing blockchain technology for clearing and settling transactions. The next stop will be blockchain settlements of virtually all U.S stock market transactions.

- The Ethereum “Merge” is now complete effectively cutting Ethereum’s power usage by 99%.

- The remaining Ethereum stages are “The Surge”, “The Verge”, “The Purge” and “The Splurge”.

“The Surge” aims to bring in a scaling solution which should complete in 2023 and reduce gas fees significantly.

“The Verge” is aimed at optimizing data storage for Ethereum nodes.

“The Purge” is a similar data optimization focused on data storage for validators.

“The Splurge” is a series of miscellaneous updates to fix any bugs from the prior stages.

- Ethereum edged closer to taking a bite out of the $138B in annual fees that the Mastercard-Visa duopoly earns. Credit card fees are the second biggest expense for U.S. businesses following payroll.

- There is a school of thought that Ethereum has sold out on the principles of blockchain with the move to PoS (Proof of Stake). One of the concerns is that a blockchain heavily reliant on DeFi for its use case is heavily dependent on the centralized stablecoin custodians. The stablecoin custodians can effectively choose their preferred chain by not supporting liquidity on other viable chains, hence starving the other chains. Liquidity trumps voting rights. Refer to the “Market in Pictures” section below for a visual illustration of the point.

- Gucci became the first luxury brand to accept in-store payments of Bored Ape Yacht Club, affiliated ApeCoin (APE), in the U.S.

- Dapper Labs launched the NFT collectibles platform, NFL All Day.

The Sheriff & Co:

- The new political leaders of both the UK and Canada stated their intentions to become countries of choice for innovators in the crypto space.

- The White House report “Climate and Energy Implications of Crypto-Assets in the United States” estimated the total global crypto electricity consumption to be between 0.4% to 0.9% of total annual global production.

- Initial Coin Offerings are back in South Korea, regulated and institutionalized as its new crypto regulations take effect.

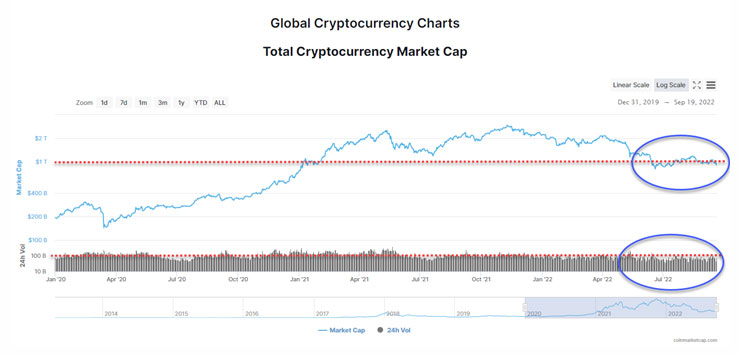

Market in Pictures

The chart below tracks the Market Capitalization of the total crypto market. Notice how the market capitalization has been oscillating around the $1T mark while volume has been decreasing. Will market cap break to $500B here or rally to $2T again?

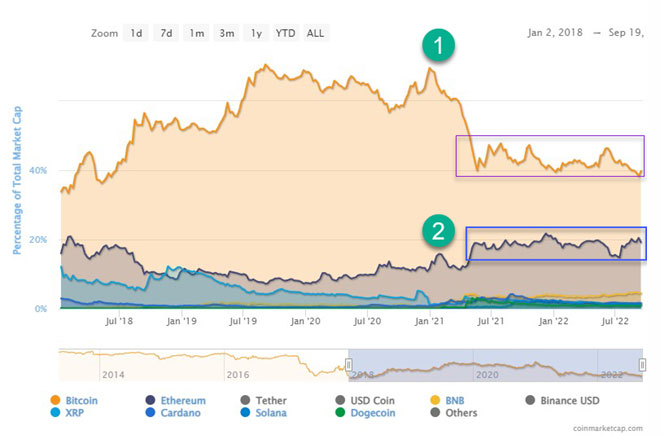

The chart below zooms in on the main non stablecoin market cap contributors. BTC is hovering around 40% and ETH at 20%. Notice how BTC’s market cap dominance peaked close to the November 10th, 2021 high and how it has decreased significantly from around 60% to around 40%. ETH dominance has made new highs since the November 2021 high and is oscillating in a higher range than its price peak.

Courtesy of coinmarketcap.com

The next chart shifts our focus to the combined market cap for the 3 largest stablecoins: Tether, USDC and BUSD, which is just short of 15% now. Historically, this is high but it did not make a new high in the most recent month. This may be the result of funds leaving the crypto environment altogether or funds being deployed into riskier assets on sale.

Courtesy of coinmarketcap.com

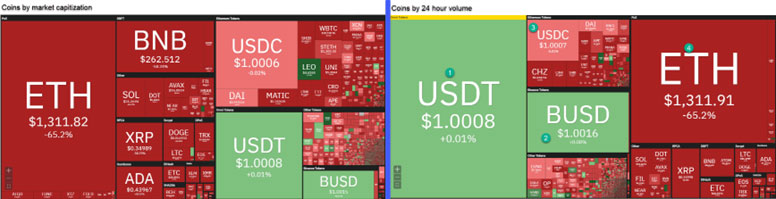

How much power and influence do the stablecoin custodians yield over the blockchains that have a DeFi use case? Traders and businesses generally want to move their funds to a specific chain or coin in a “safe” way. Safe is normally a function of their functional currency (yes, accounting pun intended). For most, the functional currency is either a fiat currency or a stablecoin linked to fiat. Therefore, we can use stablecoin volume as a proxy of the power stablecoins yield over PoS chains.

Visually, the following graphic represents that relationship (excluding BTC which uses Proof of Work):

- The size of the box on the left-hand side represents the market cap.

- The size of the box on the right-hand side represents the 24-hour volume.

- ETH, in terms of market cap, exceeds USDT, BUSD and USDC.

- On the basis of volume, USDT alone exceeds ETH. The combined total volume of USDT, USDC and BUSD is almost double that of ETH.

- If USDT decided it’s not backing a forked chain on ETH, the chain will most probably die without liquidity. In a proof of work world, this decision is solely in the hands of the miners. In an ETH 2.0 world, however, there appears to be a new king maker.

Courtesy of coinmarketcap.com

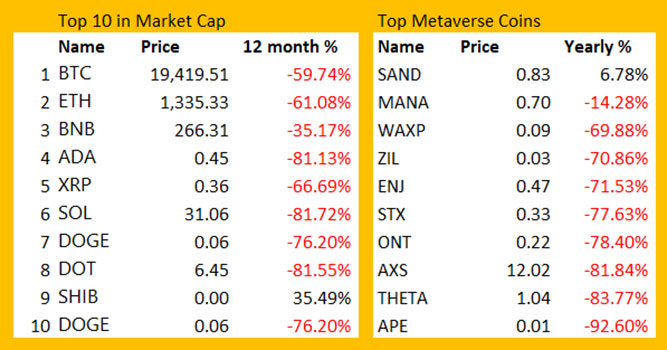

The table below shows the best and worst cryptos in terms of their Market SQN score. Of the 100 cryptos that we track, 57 are bearish, 20 are very bearish and 15 are neutral (sideways). Notice out of the top 15 there are now 8 bullish symbols while the rest are neutral. Although the overall market is bearish, this is a positive shift as the number of bullish tokens doubled from last month. Potential green shoots during the rainy season?

Also notice BTC is the third worst performer. ETH, although not on the top 15 worst list, still has a negative SQN of -0.12

On a 12-month rolling basis we see only two coins positive: Shiba Inu (SHIB) in the Top 10 Market Cap positive and The Sandbox (SAND) in the Metaverse coins. The red dragon still rages.

Overall Commentary

This is a free newsletter to the VTI community. It’s not about making any recommendations for what to buy or sell or hold. Instead, this newsletter is about understanding how money can be made in crypto assets.

Until next time,

Enjoy your own game!