Bull Normal Market Type Market Update June 30th, 2023 By, RJ Hixson

If you would like to read this article in a downloadable pdf format, click here.

If you would like to read this article in a downloadable pdf format, click here.

Just past the summer solstice, the month of June and second quarter ended last Friday—the halfway point for the calendar year. Yes, the S&P market type is “Bull Normal” but that’s not half of the story.

Part I: The World Market Model

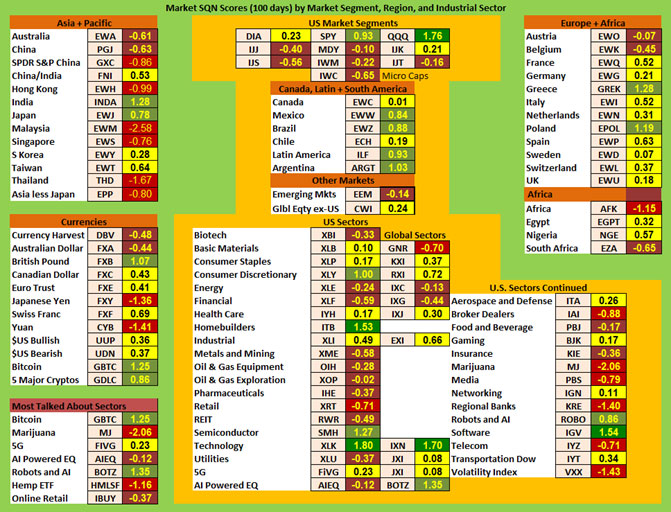

Let’s look first at Market SQN scores for equity markets across the globe and the various asset classes.

- The US market has a very strong large cap growth segment (QQQ) and a moderately strong S&P 500. But most of the segments are negative with scores weakening from May across the board.

- Outside the US, America’s other markets are stronger and mostly green now.

- Europe’s markets are almost all positive, though yellow scores dominate the region. You might remember the vitality of Europe’s mostly green scores a few months back.

- Africa runs from yellow to red – no green.

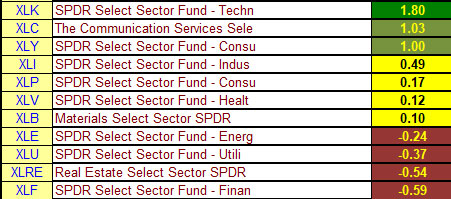

- US sectors are a mixed lot like last month. We find strength in tech-related symbols, builders, and in the consumer discretionary ETF. We also see weakness in retail, broker/dealers, marijuana, media, regional banks, telecom, and volatility.

- The Bitcoin symbol GBTC is the strongest currency with a positive USD ETF, but weak. The USD Index chart further below shows the Dollar at the high end of a sideways range.

- Asia Pacific continues to display weakness overall. Post-lockdown-China doesn’t appear to be doing much recovering. India and Japan are green, but only three other country markets are positive. The rest have negative Market SQN scores with Malaysia and Thailand being among the lowest scores in the whole database.

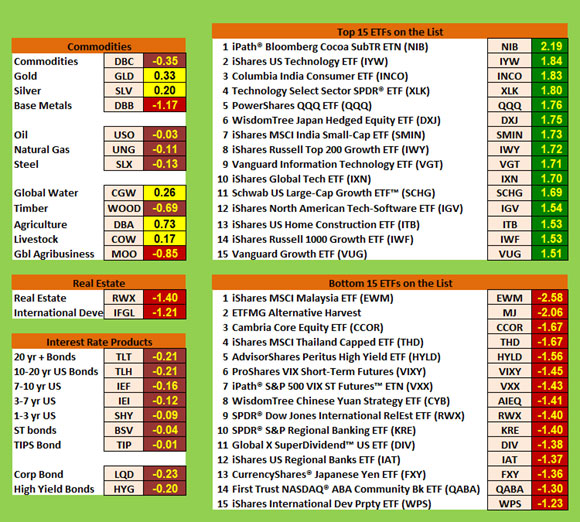

Commodities are about the same as they were last month—mostly weak. Natural gas (UNG) was one of the weakest symbols in the database a month back, but now it’s not so low. Bottoming signal or just sideways from here? Check your beliefs.

Bonds stayed unanimously brown and the two real estate issues went red.

Tech and growth symbols dominate the Top 15 List again for June as they did in May. India, Japan, and homebuilders also made the top list.

Malaysia, marijuana, and a few banking symbols are the low scorers on this month’s Bottom 15 list. So are an interesting mix of other areas—volatility, Yuan, Yen, and real estate.

The categories among the entire database shifted little in June, and the distribution still has a bearish bulge. All of the percentages are within a point or two of last month’s split.

- Very Bullish – 3%

- Bullish –10%

- Sideways – 31%

- Bearish – 44%

- Very Bearish – 12%

Part II: The Big Picture

As we kick off the second half of 2023, what do we see in the macro picture? Broad moderate to flat growth, modest stability, paused rate hikes in the US, great hopes for AI having economy scale effects, simmering geopolitical tensions, mild uncertainty . . . so, only AI is exciting but nothing is very scary presently. All of this produces a very strong tech sector bull and an S&P 500 Bull Normal market type which will probably turn into Bull Quiet in the next week or so. The rest of the equities market and other asset classes, however, are in different market types. There’s more on this point below.

Part III: The Current Stock Market Type is Bull Normal

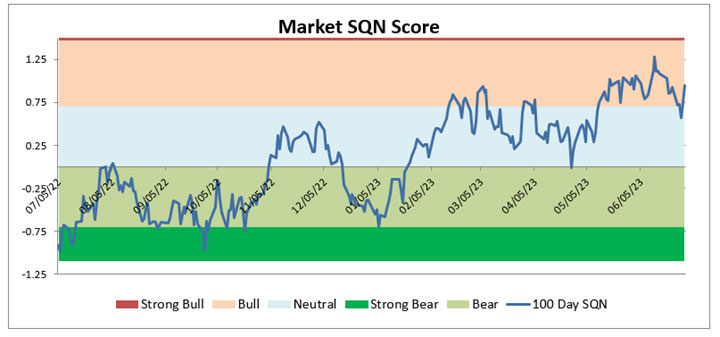

The market type direction for three of the four periods we monitor is now Bullish.

200 days – Sideways (and just on the cusp of turning Bull)

100 days – Bull (Bull last month too)

50 days – Bull (Bull last month also)

25 days – Strong Bull (Sideways last month)

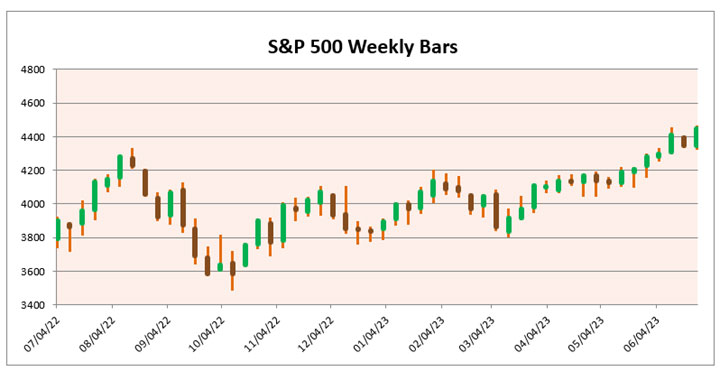

The market has been trending strongly since late last year.

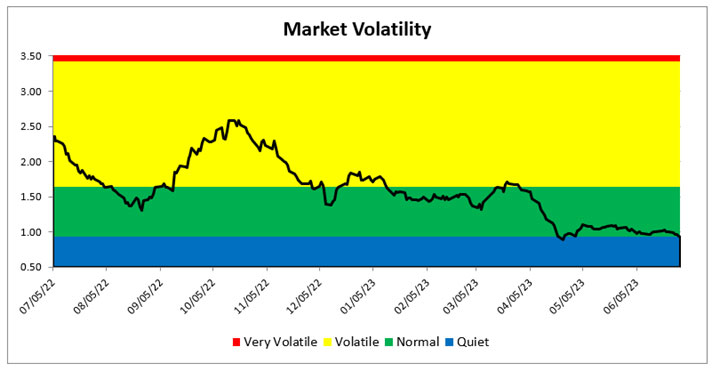

The Market SQN chart below shows the score pushing higher since early May, putting the line solidly in the bullish zone.

The 20-day ATR% has been bouncing along in the lower range of normal but may be just a few days away from turning quiet.

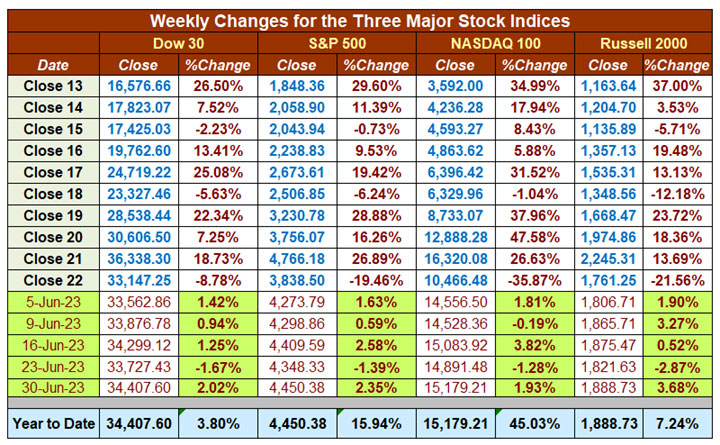

Halfway through 2023, the index’s performance ranges from modest to astronomical. Tech is 3X ahead of the next highest index—the S&P. Have any of your systems or positions been reaping the rewards of the tech sector?

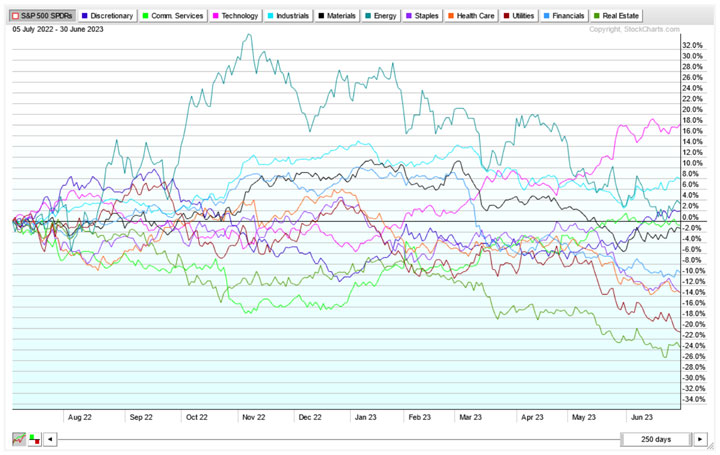

A few weeks ago in our Systems Development workshop, D.R. Barton provided his big picture view and presented a relative performance chart of the S&P sectors. A similar chart below graphs the relative annual performance of each sector in relation to the S&P, which is basically the zero line horizontally. What do you see?

Look below the zero line to see five sectors well below the index performance. There are four sectors within two percentage points of the index. The industrial sector is performing better than the index but look at that magenta line. Tech is way ahead, relative to the S&P.

Indeed, if we look at a shorter term measure, the 100 day Market SQN, those scores paint a similar picture.

Granted, different sectors perform differently at any given point in a market cycle. Because the S&P is cap-weighted, however, a few mega-cap tech companies are doing really well right now, which has a significant effect on the index number. Most stocks are not in Bull Normal mode. That’s neither good nor bad, just something to incorporate into your big-picture view and trading system selection.

Part IV: Van’s Four-Star Inflation-Deflation Model

The model went from mildly deflationary in May to mildly inflationary in June.

Gold and BTC are diverging again in performance. Van added BTC to the model a few years back as gold seemed to ignore market risk situations and inflation. He wondered if BTC had replaced gold as a preferred value and security asset. The jury may still be out on that shift so we’ll leave BTC in the model for now. BTC seems to have become more of a risk-on asset which has been correlating highly with tech in the last few years.

Part V: Tracking the Dollar

The USD Index continues trading sideways between two relatively flat MAs of 200 days and 50 days.

Conclusion

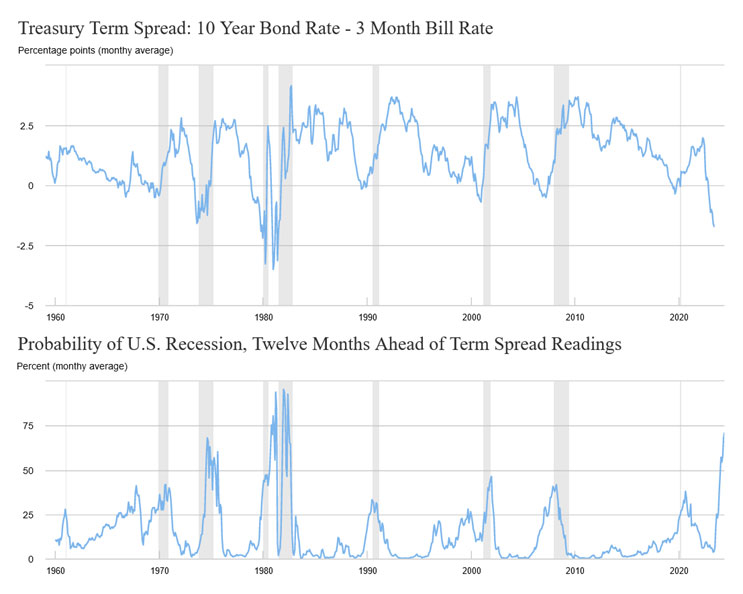

Weren’t we supposed to be in a recession by now?

That was the consensus a few months back from lots of analysts.

Perhaps the Fed finally birthed a unicorn—the fabled soft landing. Maybe . . . but one of the Fed’s own models squashes that fantasy by putting pretty high, and increasing, probabilities on a recession.

The upper chart shows the biggest spread (inversion) in yields since 1981. The lower chart shows the probability of a recession getting over 50% in December 2023.

Could it be different this time? After all, the market is in Bull Normal mode today and set to become Bull Quiet. That kind of market behavior hardly predicts a recession, does it?

And if there is a recession, does that spell a bear market? History says probably—there is a high correlation. Would that hit tech hardest, not affect tech, or would everything go down in unison?

There are all sorts of possibilities and we can play the macro scenarios game until the non-GMO cows come home. It can even be a bit of fun.

For great trading, however, we don’t have to worry, predict, or even forecast. We need to trade the systems that fit the current market type, follow their rules, and prepare for the possibilities coming up. You can make trading a lot more complex than it has to be.

Trade well and see you in August, if you aren’t on holiday.

P.S. We’d like to acknowledge a piece of software used in the production of Van’s World Market Model and the Market SQN charts. The Excel plugin, called XLQ, essentially eliminates the work of importing price data from multiple sources and calculating technical indicators. There’s a free trial of up to 45 days and Van Tharp Institute clients get a nice discount by using the discount code “IITM” in the checkout process. VTI receives no financial benefit from anyone purchasing XLQ. We simply mention the software to you because XLQ has proven to be a highly useful and dependable tool for us – and for many of our clients – over many years. We are grateful.

You can find more information at https://qmatix.com/index.htm