Multiple Banks Collapse and U.S. Equities Markets Go…Up?!? By, D.R. Barton, Jr.

In the wake of the sudden Silicon Valley Bank collapse (followed by other banks in the U.S. and abroad), a surprising resilience has emerged within the U.S. stock market. Defying the naysayers, the market has not only weathered the banking storm so far but has also produced positive returns just a little more than two weeks into this financial reckoning.

In the wake of the sudden Silicon Valley Bank collapse (followed by other banks in the U.S. and abroad), a surprising resilience has emerged within the U.S. stock market. Defying the naysayers, the market has not only weathered the banking storm so far but has also produced positive returns just a little more than two weeks into this financial reckoning.

There are two short-term money trends that help us understand this rebound and two associated indications that will point to whether the market can keep up the revival, or if it will lose its footing heading into the summer. Let’s dig into them all.

Where is the Fear?

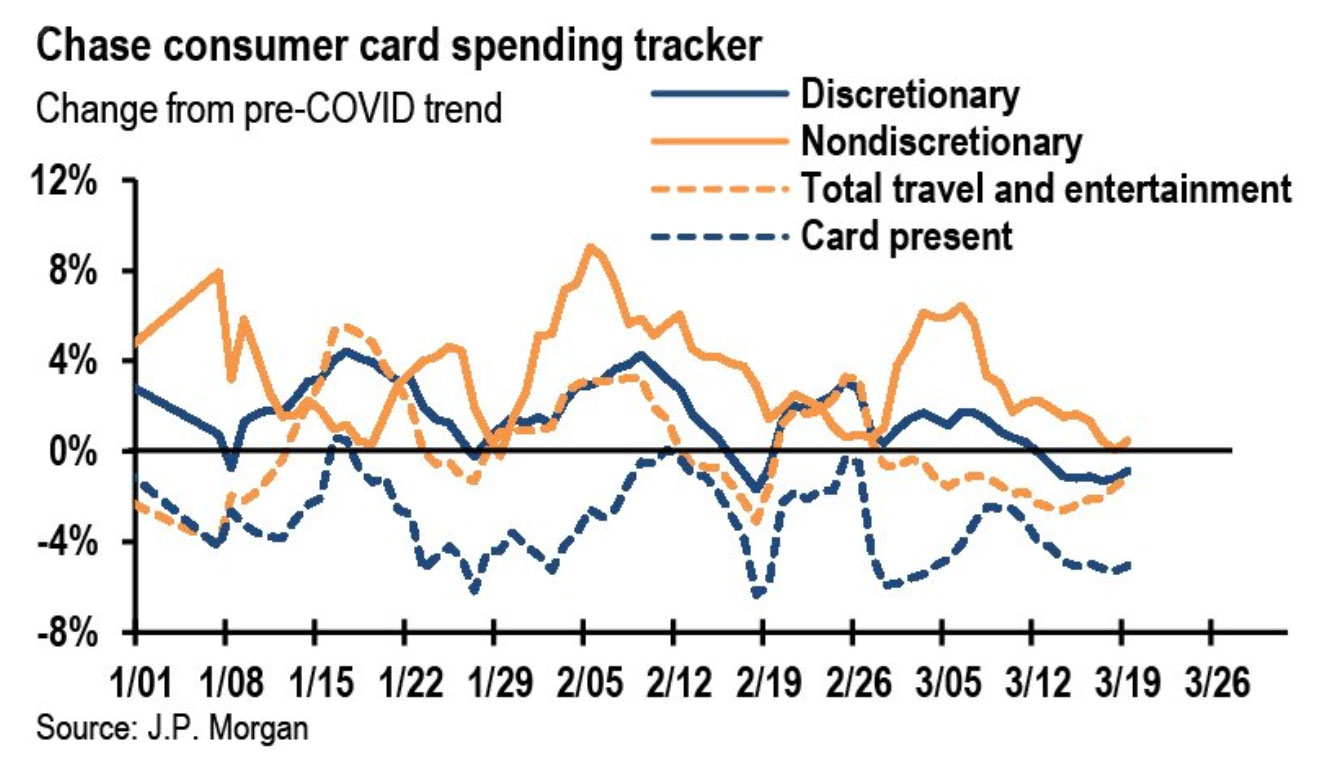

Late last week, JP Morgan pointed out that “Recent bank failures in the US have raised questions about the consequences for consumers… our Chase consumer card transactions data (credit and debit) through March 19 do not show a meaningful impact on spending in the first week after the event.”

The chart shows that small downtrends from the first few days of the crisis were turning back up, heading into the second week after the SVB debacle.

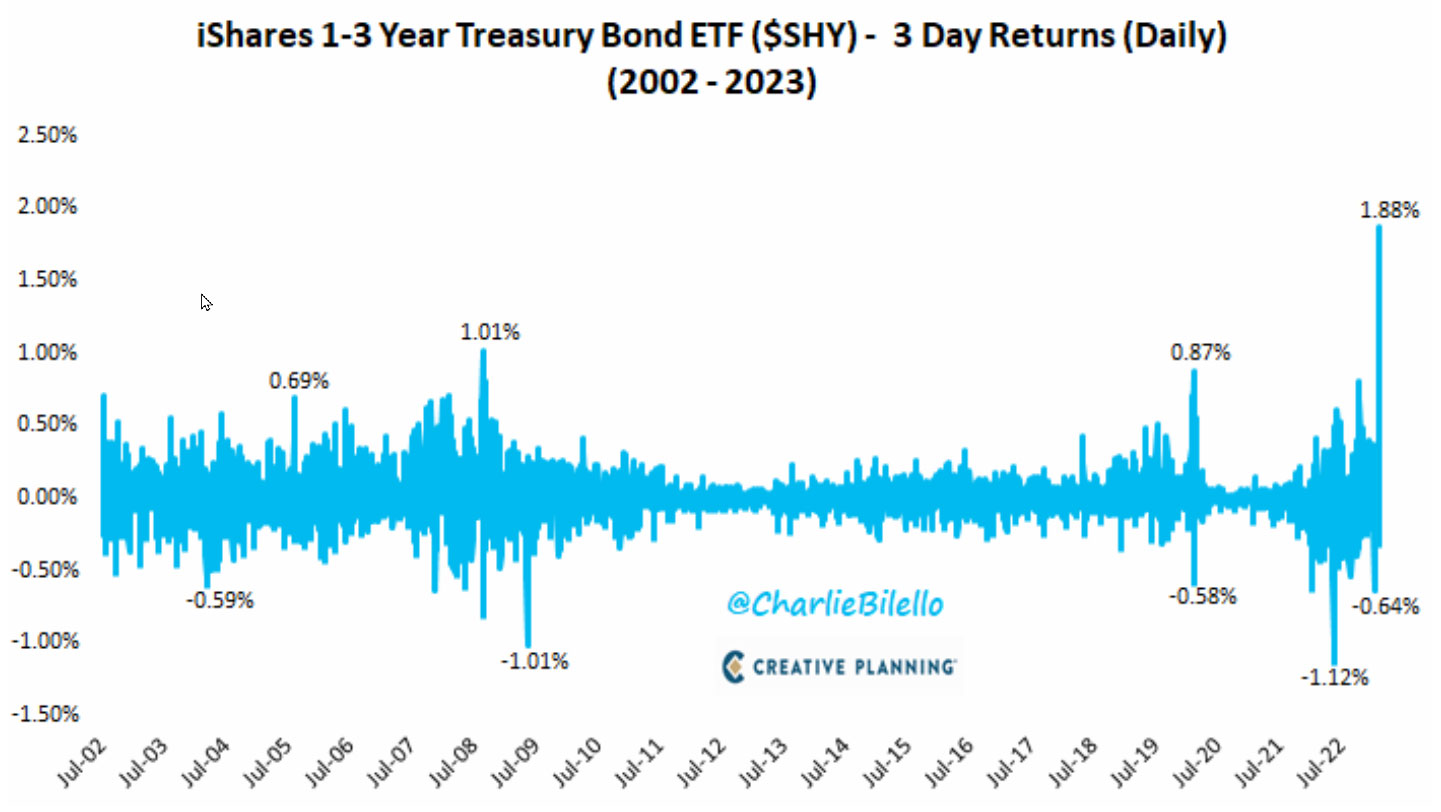

The second point is that we can see where investors fled with their cash when we saw prices in short-term bonds skyrocket in the biggest average three-day move of the last 20 years (as yields collapsed):

This second item of short-term yields dropping precipitously shows the underlying cause that has given the market a tailwind—the perception that the SVB and other bank collapses have done the Fed’s job for them. This means that the banking problems will bring about enough economic uncertainty that this will further slow the inflation freight train so that the Fed can stop hiking rates in the near term.

The Question Is: Can Equities Hold Ground or Gain Even More?

This is certainly one of those times when the winds of uncertainty are blowing, but it is clear that investors find themselves seeking the relative safety of cash. When a substantial amount of investable money is withheld from the markets, it can lead to a unique set of consequences that are worth exploring.

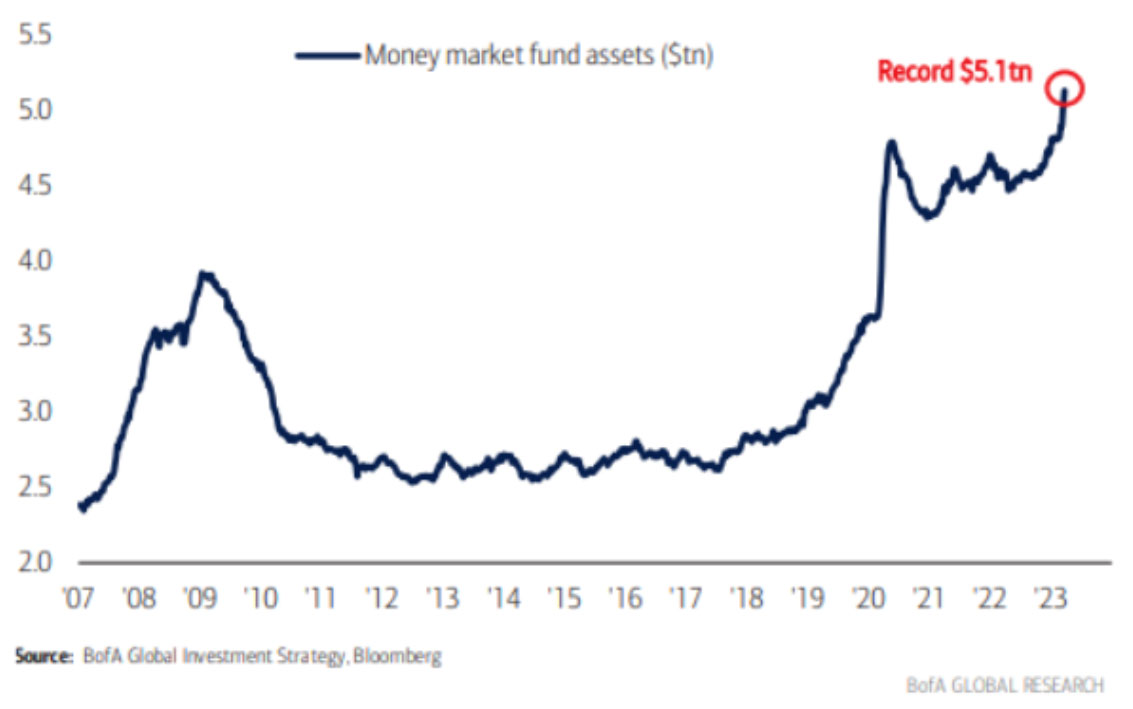

In a recent Bank of America global fund manager research report, it was revealed that a record amount of assets has found their way into money market funds, showing that even though consumers are still spending, collective apprehension has played out among investors:

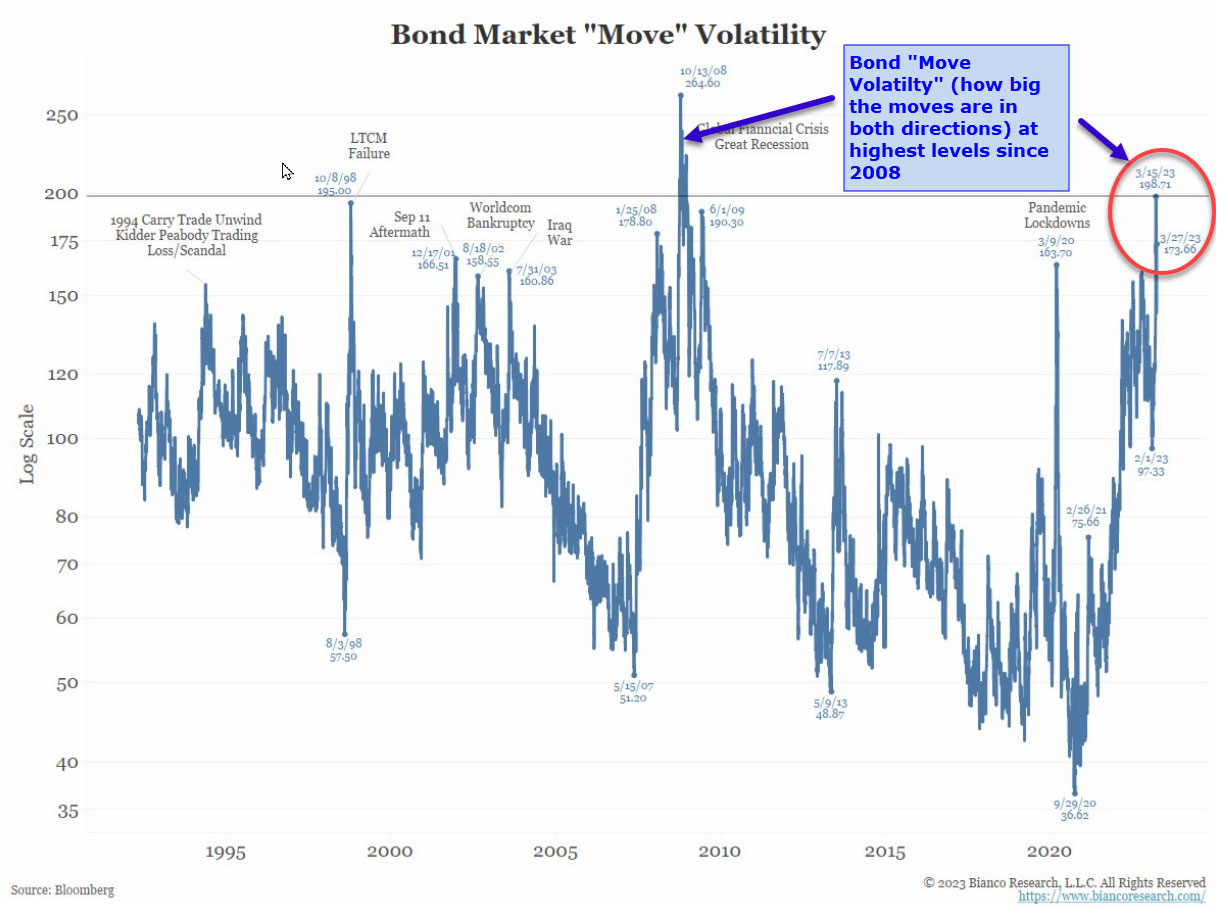

There is now a record $5.1 trillion seeking the relative safety (and admittedly higher yields) of money market funds. The ever-insightful Jim Bianco, of biancoresearch.com, shared this chart. It shows the uncertainty in the bond market right now that is leading to near-record levels of price volatility:

This brings us to the two things to watch going forward.

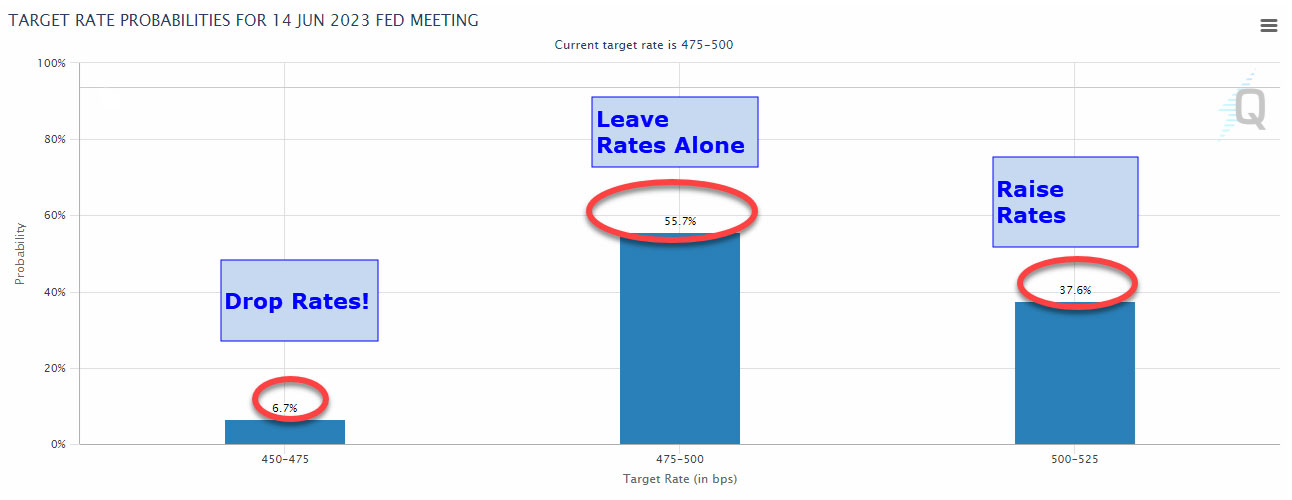

The first is the reason for the volatility in the bond chart above. We’ve reached what Jim Bianco calls “complete confusion” over what the Fed will do next. Bianco cites the tool that I’ve been writing to you about for years. The one that reflects the futures positions of traders who are hedging other positions or speculating on the FOMC outcomes—the CME Group FedWatch Tool:

As you can see, even on Tuesday, March 28th, some traders think that by the June meeting, the Fed will either:

- Hold rates the same (56%),

- Cut rates (7%), or

- Hike rates (38%)

It’s very unusual for institutional traders to price all three options for the same relatively close Fed meeting. Hence, the market confusion and extreme moves.

If the probability for a cut is eliminated by the market participants in the coming weeks and months, then the strong upside for the markets heading into the summer is much less likely.

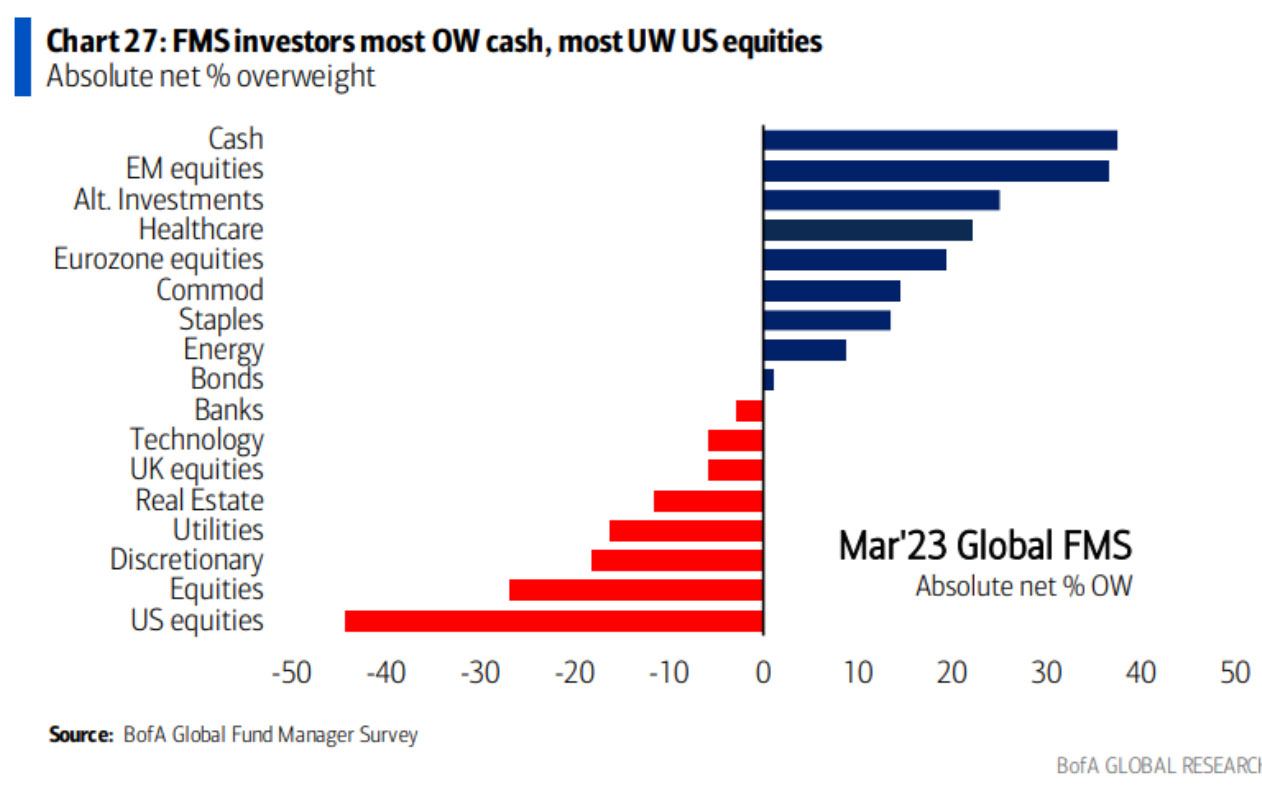

The second thing I’m watching also comes from the Bank of America global fund manager survey (that I reference in the money market fund cash chart above). Right now, cash is the most held asset—overweight (OW) while US Equities is the least (underweight or UW):

What happens when investor sentiment reaches extreme levels (and I really don’t think it can get too much more negative on U.S. Equities)? When too many folks get on one side of the boat, they can’t stay there very long.

Markets can be slow to react to extreme sentiment. And sentiment alone is not a very reliable timing mechanism. However, it’s this combination of overblown sentiment and record levels of cash in liquid money market funds that can fuel more movement to the upside in the short and intermediate terms, regardless of whether or not you think we’re going to get another big move to downside this year.

Are the bank runs and collapses over, or just getting started? Are you surprised that the equities markets are proving oddly resilient in the face of the banking troubles? Let me know!

I always enjoy hearing your thoughts and comments. Send them to me using drbarton “at” vantharpinstitute.com.

Great investing and God bless you,

D.R. Barton, Jr.