The Power of The Right Financial Structure: A Pathway to Enhanced Freedom By, Mark Boucher

Financial freedom is an aspiration held by many, yet fully realized by few. One key to achieving this elusive goal lies in understanding and leveraging financial structures effectively. The difference that can be made by making small shifts in how one handles their financial structures is immense, and it directly affects how much money you can set aside, as well as how rapidly the money you do set aside can compound. Most people are restricted by what they can invest in via the tax-advantaged structures they have set up (like IRA’s, 401k’s, and Solo 401k’s). But in many cases there are ways around most restrictions people face, if setup properly. The ability to transition from a restrictive financial structure to one that offers more freedom can be worth a fortune and can speed up and simplify the building of your financial fortune.

Financial freedom is an aspiration held by many, yet fully realized by few. One key to achieving this elusive goal lies in understanding and leveraging financial structures effectively. The difference that can be made by making small shifts in how one handles their financial structures is immense, and it directly affects how much money you can set aside, as well as how rapidly the money you do set aside can compound. Most people are restricted by what they can invest in via the tax-advantaged structures they have set up (like IRA’s, 401k’s, and Solo 401k’s). But in many cases there are ways around most restrictions people face, if setup properly. The ability to transition from a restrictive financial structure to one that offers more freedom can be worth a fortune and can speed up and simplify the building of your financial fortune.

In the United States, the most commonly used and tax-advantaged financial structures are retirement plans, particularly for working-class Americans. Indeed, studies show that without retirement plans, most Americans would have very little savings. The typical American stores savings in two primary areas: the equity in their home and the equity in their retirement accounts. Among these retirement accounts, the traditional Individual Retirement Account (IRA) and the Roth IRA, along with the traditional 401k and Roth 401k, are the most prevalent. Although the Solo 401k, and Solo IRA can often be funded much more quickly and substantially.

Choosing between these options can be based on various factors, including whether your company offers both, and whether you are self-employed or have a part-time business. However, it’s worth noting that most companies traditionally offer only the conventional 401k. Despite their prevalence and simplicity, most of these traditional 401k retirement accounts have very limited flexibility, exceptionally high fees and, therefore, mediocre performance. Funds are deposited, but returns are minimal, creating a problem for investors.

At first glance, the beneficiaries of retirement accounts seem to be the retirees or the workers themselves. However, upon closer inspection, it becomes apparent that in many cases the primary beneficiaries are financial service firms like Fidelity, Vanguard, BlackRock, Charles Schwab, Franklin Templeton, and Pimco. These non-optimal retirement accounts serve mainly as fee generators for Wall Street, which charges unusually high and multi-layered fees for most products and limits the investment choices so severely that an investor is stuck without much chance of achieving decent performance to compound this wealth source.

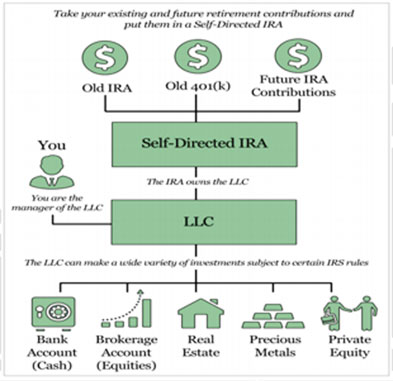

Most traditional 401k plans are heavily dependent upon stock market returns for their performance. A mix of stocks and bonds, both with very high fees eating away at them, usually comprise all the options 401k holders have. But structured correctly, Solo 401k’s, Solo IRA’s, Rollover IRA’s or Rollover 401k’s that were managed by a former employer or of an independent business owner, can be structured to avoid all these problems. Self-directed structures allow investments into precious metals, commodities, forex, options, futures, mortgages, oil and gas partnerships, real estate, and higher-frequency trading strategies that allow for more diversification. And stronger potential returns can be traded by an LLC owned by your IRA or Solo 401k as its main investment. You can reduce fees and take charge of your retirement funds. And proper structuring can greatly increase the amount put into these tax-free vehicles as well.

Despite the challenges, it is possible to overcome the severe limitations of traditional 401k’s and IRA’s to create a financial structure that maximizes money funneled into the structure, and then promotes higher compound growth, control, flexibility, and security. One key strategy shifts your traditional financial structures into Self-Directed retirement vehicles and LLC’s within them that allow for a broader array of investment options than a traditional IRA or 401k plan.

True diversification comes from having investments in different asset classes beyond just stocks and bonds, because there are periods such as higher periods where both bonds and stocks fall at the same time, as they did in 2022 and during much of the 1970’s.

The Solo 401k offers similar advantages to a Self-Directed IRA SDIRA, but it has a larger contribution limit, and it allows for personal loans up to 50% of the plan value. You can contribute up to $66,000 for you (and the same amount for your spouse) per year of pre-tax income from self-employment into a Solo 401k. And if you are over age 50, that amount rises to $73,500 per year (and again same amount for your spouse for up to $147,000 of pre-tax income put into it a year).

Regardless of whether you choose a SDIRA or a Solo 401k, it is essential to make your money work for you instead of someone else. Actively managing your investments and aligning them with your financial goals can provide you with a higher return on investment and increase your chances of achieving financial freedom.

Of course, there are risks to taking control of your retirement structure—you are responsible for your investment choices and trading, and for keeping up with the tax implications and the legal rules associated with these accounts. Any missteps could lead to tax penalties or legal issues. Therefore, you should consider working with a tax advisor or a financial advisor to ensure you are following all the rules and making informed decisions. And you should only be investing in proven strategies with a solid long-term track record.

While the transition from a restrictive financial structure to a more flexible one may seem daunting, it can be one of the most important shifts you make in your financial life. You may discover investment opportunities you were unaware of and develop new financial skills. With the right tools and guidance, you can harness the power of financial structures to your advantage and work towards financial freedom.

“Anyone may so arrange his affairs so that his taxes shall be as low as possible; he is not bound to choose that pattern which will best pay the Treasury. There is not even a patriotic duty to increase one’s taxes.” – Judge Learned Hand

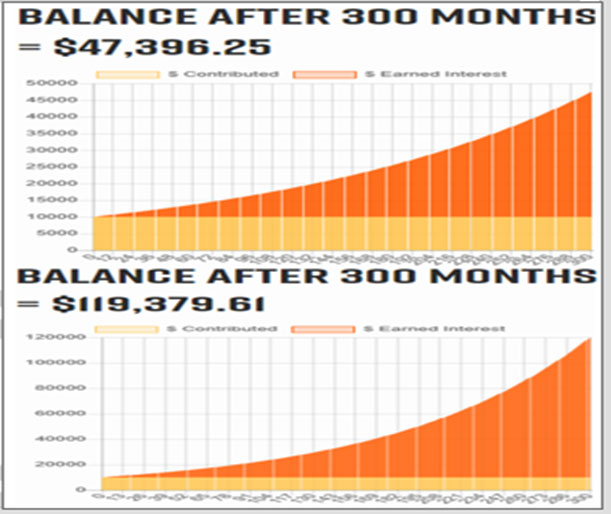

$10,000 turns into 2.51X more after 25 years when paying taxes versus avoiding them, assuming just a 12% average annual return and a 20% tax rates

In our upcoming June 22nd financial Freedom Accelerator workshop we work with proven professionals to teach you what your options are, how to setup retirement structures that will maximize the amount you can to put into tax-free or low-tax structures, how to design those structures so you can implement top investment strategies in them with optimal flexibility, and who to work with to maximize the benefits of compound growth in these structures.

Always remember, the power of your financial future is in your hands. Choose wisely, invest wisely, and grow wisely. Achieving financial freedom is not just about having wealth; it’s about having flexibility and control over your financial destiny.